Market Reality: A Turbulent Operating Environment

In 2025, U.S. hotel performance is shaped by unpredictable demand shifts, global unrest, staffing instability, and a patchwork of federal policies that continues to disrupt travel flows and pricing power. International arrivals have declined across key source markets.

As of July, travelers from Germany, Spain, the U.K., and Canada are down by double digits year-over-year, with overall inbound volume falling by nearly 12 percent. Visa processing delays, fluctuating travel advisories, and macroeconomic anxiety are just a few of the contributing factors.

Federal policies are also affecting domestic transient travel. Government travel restrictions, reduced department budgets, and postponed meetings have chipped away at occupancy in major urban markets. Washington D.C., in particular, has seen a pronounced slump. These federal influences are compounding inflation, labor shortages, and rising ownership costs, creating an environment where topline success is no longer enough to ensure profitability.

Profit and Revenue: Separate Metrics, Shared Destiny

The traditional model of optimizing revenue without deeply integrating cost considerations is no longer viable. Profitability and revenue growth must be managed as part of a unified strategy. A hotel can beat budget on revenue per available room (RevPAR) and still fail to generate acceptable profit margins if it overspends on distribution, labor, or food and beverage (F&B) operations.

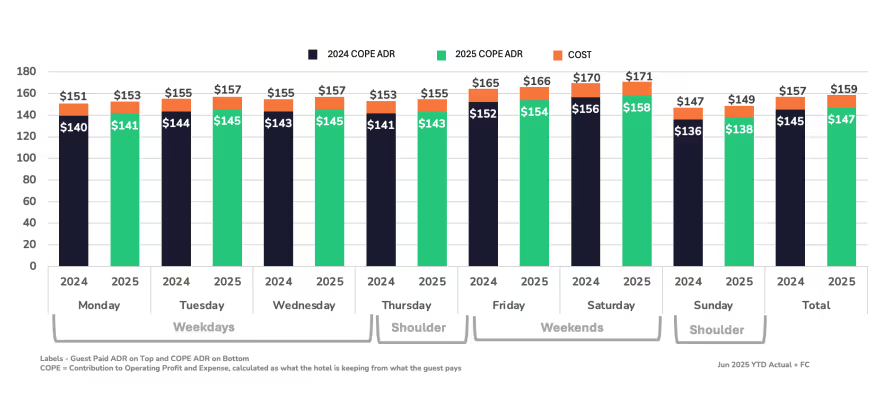

Kalibri advocates for this more integrated commercial lens. Decision makers must move beyond occupancy and rate alone. Metrics like Contribution to Operating Profit and Expenses Revenue (COPE) help identify which demand streams truly drive value, and which simply add volume without contribution.

This isn't a shift in terminology. It’s a shift in thinking. Owners and operators need to know whether that group block, long-stay rate, or online travel agency(OTA) promotion actually improves the bottom line. Without this clarity, strategy is simply guesswork.

5 Strategic Priorities to Consider

- Redefine the metrics that guide performance. You can’t measure commercial success solely by RevPAR. Hotels need dashboards that include net revenue metrics and profitability by segment, booking channel, and length of stay.

- Re-establish shared accountability across teams. Revenue leaders, sales teams, marketing, and operations should be working from a common forecast with aligned goals. When the full team understands the financial implications of their decisions, stronger outcomes follow.

- Forecast cost alongside demand. Labor, utilities, insurance, and ownership costs can erode margin if not anticipated. Build cost assumptions into commercial forecasts to avoid margin shocks after the fact.

- Treat food and beverage as a profit center, not a loss leader. Service model adjustments, tighter menu design, and selective automation can help maintain guest satisfaction while improving margin. Contribution, not just volume, must drive planning.

- Use segmentation data to drive smarter business mix decisions. Not all bookings are created equal. Understand the net profit impact of extended stay, OTA, Brand.com, and negotiated corporate business. The most valuable demand is often the most disciplined, not the most visible.

What the Data Tells Us

Kalibri’s market tracking shows that upper-upscale and full-service properties are experiencing strong revenue gains, particularly in group and premium transient segments. However, these same properties are absorbing the highest increases in labor and ownership expenses. In many cases, profitability is lagging behind revenue recovery.

Select-service and extended-stay hotels are typically more nimble. They benefit from leaner staffing models and longer lengths of stay, which help manage turnover and cleaning costs. That said, aggressive discounting or over-reliance on particular channels can quickly erode their margin advantage. Even these more efficient assets need to be selective about what demand they pursue.

A one-size-fits-all strategy is no longer practical. Hotels must understand their own market conditions, cost pressures, and demand trends at a granular level. What works in a tertiary leisure market will not work in a business-heavy urban core.

The Path Forward

There’s no doubt that economic signals remain mixed. Inflation remains sticky in some markets, while wage growth and service costs continue to climb. Federal budget cycles, foreign policy shifts, and immigration rules all add to the instability. Yet performance is possible, even in this complex environment, if leaders center their strategy on precision, adaptability, and profitability.

Commercial teams must be empowered to measure success by more than occupancy. They need access to tools that reveal which decisions lead to stronger contribution, not just fuller hotels. Strategy should reflect cost, opportunity, and timing in equal measure.

The best operators are already adopting this mindset. They’re making intentional choices about rate structure, channel distribution, staffing models, and revenue segmentation. They aren’t just reacting to market forces. They’re planning with purpose.

Profit and topline growth aren’t separate conversations. They’re two sides of a single strategy.

Hotels that fail to balance both will struggle to maintain momentum in an environment that rewards resilience and precision over volume alone